“Primum non nocere” – First, do no harm.

In our pursuit of helping:

- active money managers and investors create beta,

- management teams of industry leading companies better their competition,

- all investors of time, talent and money find ways to leave the world better than they found it.

We see our first duty as similar to the medical profession’s Hippocratic Oath, “First, do no harm.” Or translated into our profession’s primary requirement, “First, don’t invest in endeavors with no worth.”

We Offer an Intangible on an Intangible.

We Offer an Intangible on an Intangible.

You cannot take a certificate for millions of shares of FedEx to its headquarters in Memphis and exchange that certificate for a FedEx airplane. A stock or bond represents a legal right to an amount of, or percentage of, cash in the future, but investors are buying an intangible. Our advice, our data on the industry and economy, or insights to historic patterns and future possibilities are also an intangible. It is an intangible on an intangible, so our first duty is to not suggest anything that, despite perceptions to the contrary, is worthless.

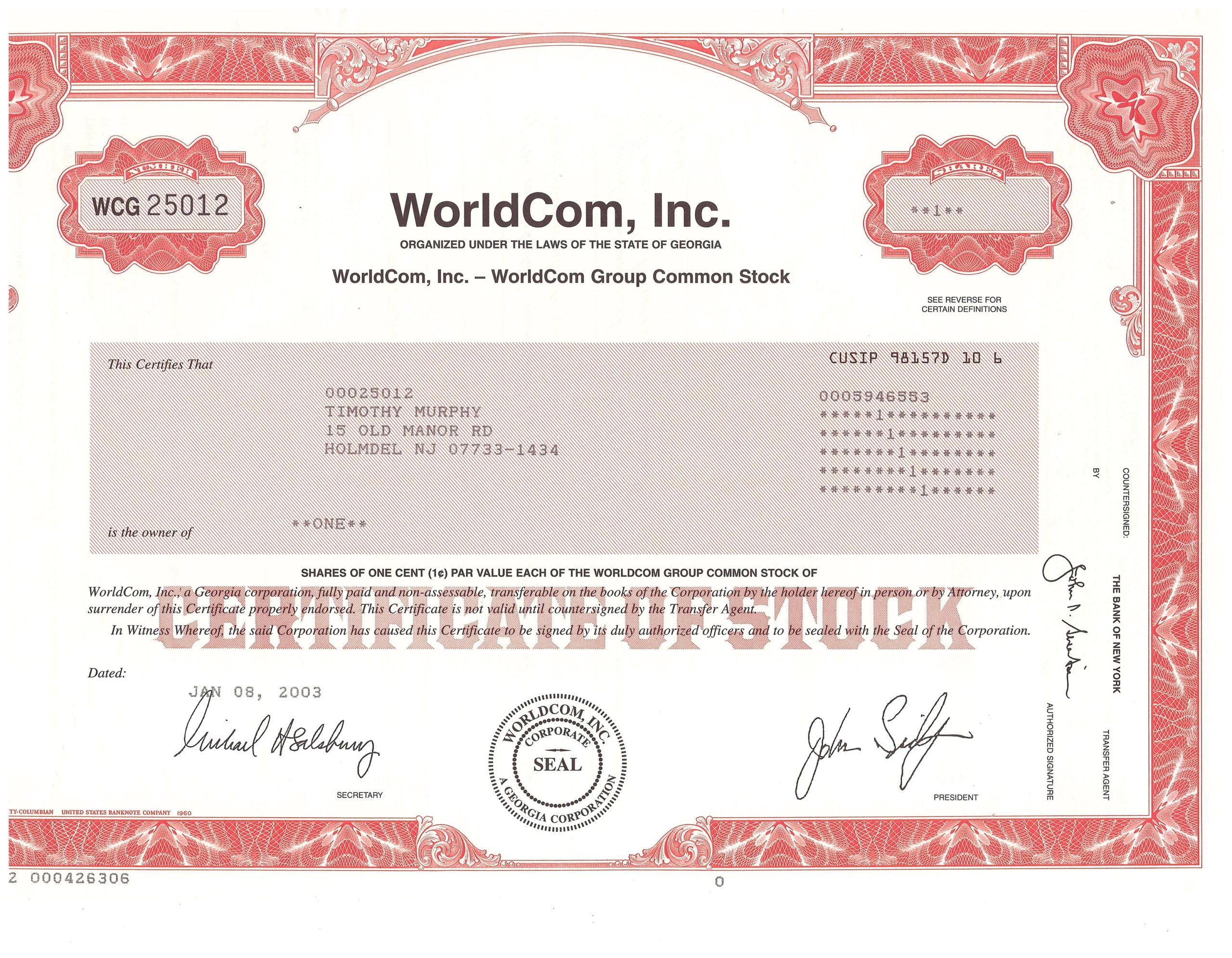

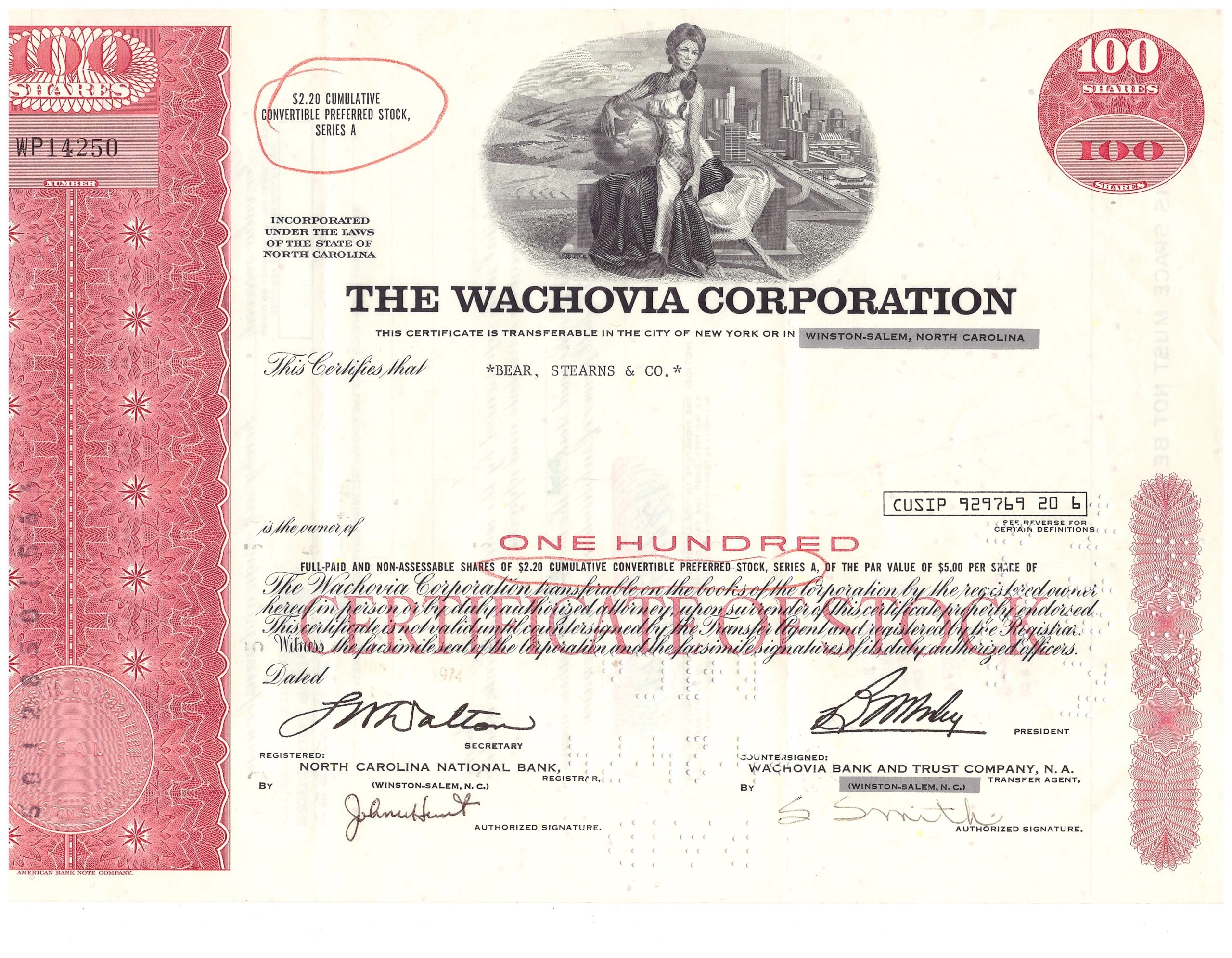

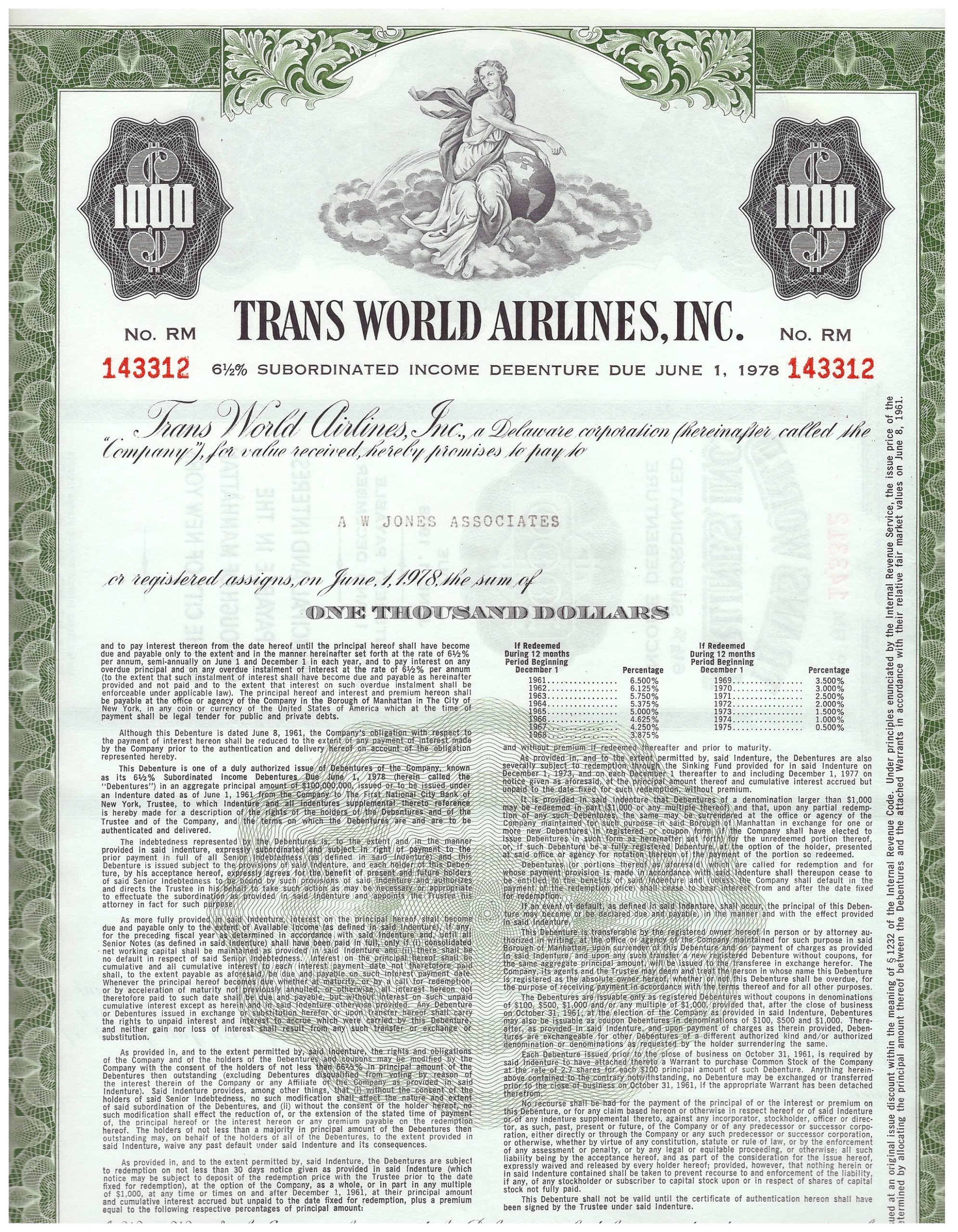

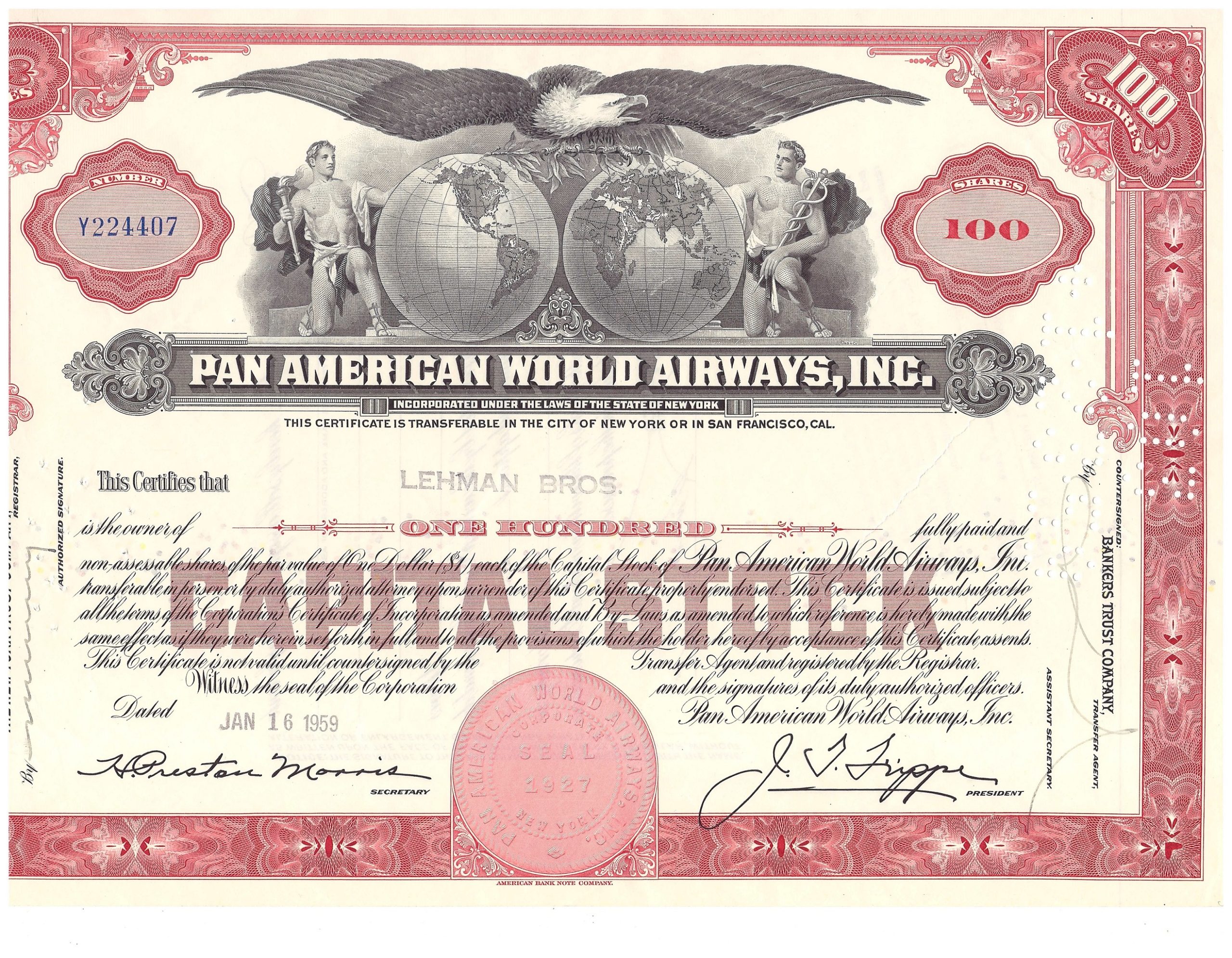

These documents are stark reminders…

Our ‘Wall of Shame’ is just inside the front door of our St. Louis offices. Framed are the stock certificates and bonds that were once thought to be valuable, but proved to be worthless. We are always looking for opportunities, while vigilantly watching for what could go wrong, as well as what we find to be untrue.

Our ‘Wall of Shame’ is just inside the front door of our St. Louis offices. Framed are the stock certificates and bonds that were once thought to be valuable, but proved to be worthless. We are always looking for opportunities, while vigilantly watching for what could go wrong, as well as what we find to be untrue.

We explain the meaning behind them, the reason for them, to every person we interview, and company or client that visits us. They also quietly remind us, as we walk past them, of the responsibility we have to investors.

Sure, some money has value in the precious metal of which it is composed.

Sure, some money has value in the precious metal of which it is composed.

But, most units of ‘hard currency’ are only valuable if they are trusted as a worthy and reliable unit of exchange.

In all of these, even the pure gold one, except during periods of severe deflation, there is no income, no growth or appreciation in value. In order to receive that reward, you must take the risk of investing in the intangible.

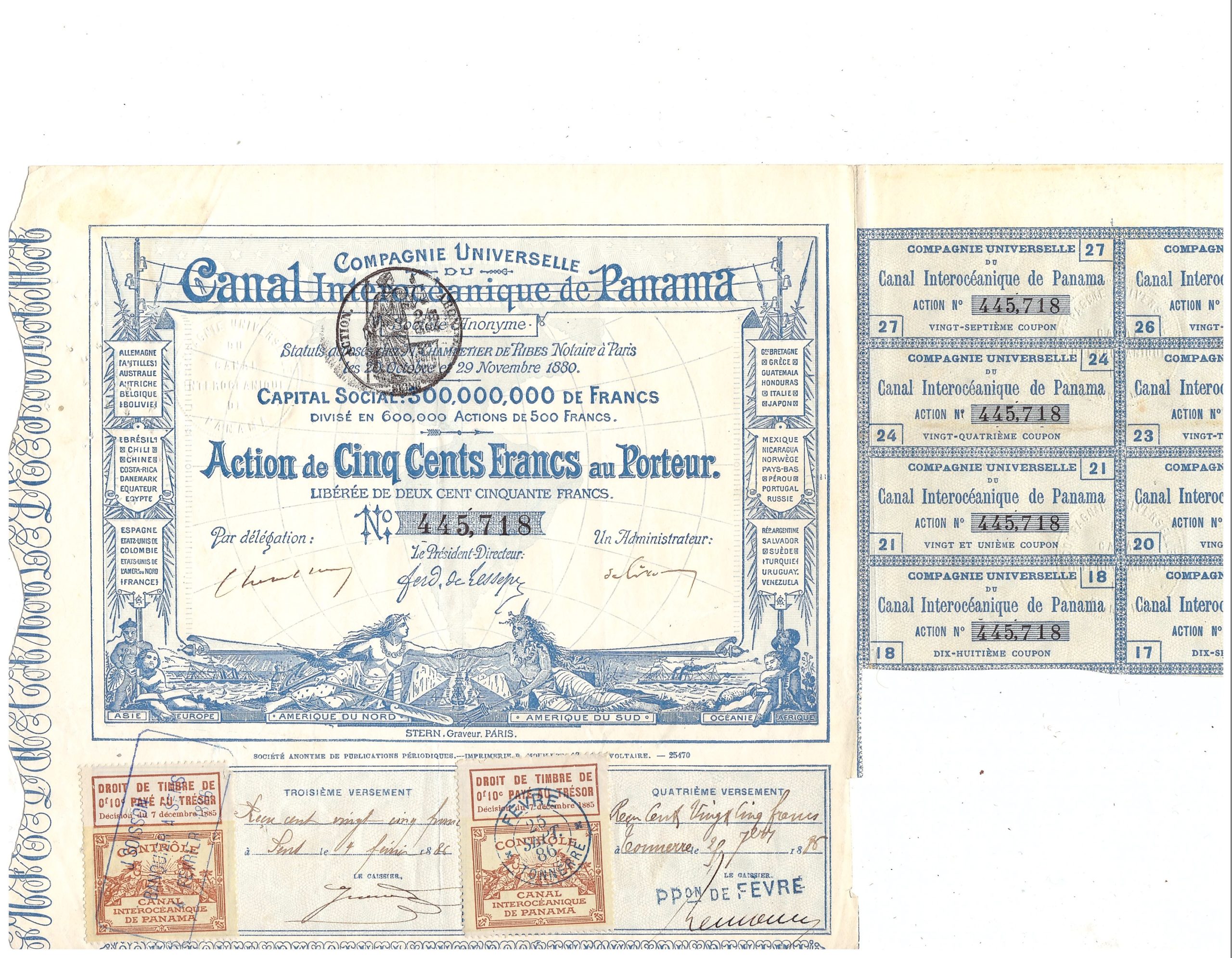

The documents in our Wall of Shame:

It was widely considered one of the most admired firms on Wall Street. After surviving the 1929 Crash without laying off a single employee, it ironically became the first of the big firms to fail in March 2008 at the beginning of the worst market panic since 1929.

They owned an unsinkable ocean liner named the Titanic. What could possibly go wrong?

A great airline! The first time I was in a plane, it was a TWA plane. The first time I flew to New York, Los Angeles, San Francisco, Miami, and London, it was in a TWA plane.

It transformed the industry from props to jets, led the expansion from narrow bodies to wide, and with IBM pioneered the computerization of airline reservations. With global reach and a brand name that was so well known it became a target. In 1988, a terrorist bomb killed hundreds of innocent people over Lockerbie Scotland, and within three years, one of the greatest airlines of all time was killed as well. Bonus points – look closely, the shares were held at Lehman Bros.

In 1864 an investor bought this $1,000 bond from the Confederate States of America. Yielding 6% a year for 30 years, there are 60 coupons which could be clipped and redeemed for $30 each every 6 months, until the principal was repaid in full. Not a single coupon was clipped. Discounted at a rate of 6%, the present value of that initial investment and over 155 years of bi-annual $30 payments is over $17.7 million in today’s dollars. These bonds are not rare, although examples such as this one, which have no coupons clipped, are not common and sell quickly when they do become available. Yet, even after all that time, despite having no coupons clipped and despite being in near mint condition, it still isn’t worth the original face value of $1,000. As Will Rodgers once quipped, “Be less concerned about the return on your capital and more concerned about the return of your capital.”